15-07-2024 | Noticias-en

By Decree No. 852 of July 5, 2024 (the “Decree 852”), the Ministry of Environment and Sustainable Development (the “MADS”) modified the environmental licensing regime for energy generation projects from non-conventional sources (“FNCER”).

What changes does Decree 852 introduce?

Decree 852 introduced the following modifications:

- Change in the powers of the ANLA and the CAR.

- Introduction of a new definition.

- Transitional regime regarding the change of powers.

Download the newsletter here .

12-07-2024 | Noticias-en

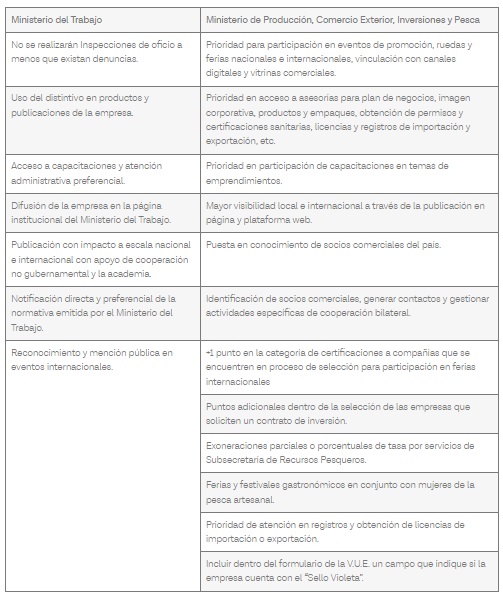

On June 11, 2024, Interministerial Agreement No. MCEIP-MDT-2024-001-AI was signed between the Ministry of Labor and the Ministry of Production, Foreign Trade, Investments and Fisheries. The new regulations stipulate that companies wishing to obtain the “Violet Seal” must take into account principles, norms, actions and indicators that demonstrate the employer’s commitment to eliminate barriers, wage gaps, situations of violence, harassment and discrimination, promotion of promotions and conciliation with care tasks, elimination of discriminatory permits and breastfeeding, as well as the promotion of equality in collective bargaining.

Both ministries announced that they will grant the following benefits to companies that obtain the “Violet Seal”:

Procedure for obtaining the “Violet Seal”:

To obtain this badge, companies must submit the following documents through the Document Management System of the Ministry of Labor:

Application form for obtaining the “Violet Seal” Distinctive.

Payroll of Workers.

Notice of Entry to the IESS of the workers.

Payment roles for the last three months of the workers.

Proof of payment of the workers’ reserve funds; delivery of supplies, instruments; delivery of clothing.

Document of not being in arrears or maintaining glosses or credit titles in the certificate of compliance with obligations issued by the IESS.

Documents that demonstrate compliance with the Program for the Prevention of Psychosocial Risks registered in the Ministry of Labor.

Comply with the equality policies and the guidelines provided by the Ministry of Labor for compliance with these.

Not having been sanctioned for a complaint from a worker due to discrimination, workplace harassment, sexual harassment at work or violence against women in the last three (3) years.

Equality Plan Registry.

Job Manual in accordance with current regulations.

Human Talent/Human Resources List that includes promotions and professional development.

Registry of training carried out in the last year.

Implementation of current regulations to eliminate harassment, violence and discrimination.

Within 60 days of submitting the documentation, the certifying entity will issue a report analyzing the submitted documentation and will decide whether to approve or deny the granting of the “Violet Seal”. Once the Ministry of Labor knows the final approval report, it will grant the “Violet Seal” Resolution and its distinctive mark.

The duration of this badge will be 1 year from the date of delivery and may be renewed for equal periods indefinitely.

Finally, the Ministry of Labor reported that it will delegate the review of the requirements and certification of this distinction to entities that meet the requirements set forth in the regulations. Likewise, labor inspections may be carried out to verify the effective application of the actions implemented in the prevention, promotion and guarantee of women’s rights in the workplace.

If you require additional information, please contact the email laboral@bustamantefabara.com

21-02-2024 | Noticias-en

Currently, ESG (Environmental, Social, and Governance) practices are becoming increasingly important. These three pillars, ranging from environmental sustainability and social responsibility to ethics in corporate governance, represent a change in how companies evaluate and conduct their operations.

ESG practices are not just isolated or complementary initiatives; They are becoming essential components of business strategy. Its integration into the business model is a reflection of a more conscious and responsible approach towards a company’s operating environment, its community and its internal processes. In this sense, ESG represents an evolution in corporate thinking, where sustainability and social responsibility are seen as indispensable factors for business success and longevity.

This growing relevance of ESG practices in the corporate sphere is due to a combination of factors. On the one hand, there is a broader recognition that business activities have a significant impact on the environment and society. On the other hand, consumers, investors and regulators are increasingly demanding that companies act responsibly and transparently. Thus, the adoption of ESG practices is becoming a distinctive element for companies that seek not only to excel in their field, but also to contribute positively in the area in which they operate.

What are ESG Practices?

ESG practices, an acronym for Environmental, Social, and Governance, represent a set of criteria that companies use to guide their operations and policies in a way that is socially responsible, ethically managed and environmentally sustainable. These criteria not only reflect corporate responsibility, but can also significantly influence the long-term profitability and sustainability of a company. For clarity, below is a breakdown of each component and practical examples of how they are applied in the corporate environment:

Environmental: The environmental component focuses on how a company interacts with the environment. This includes managing natural resources, reducing pollution and carbon emissions, and developing sustainable practices. For example, a company could implement policies to reduce its carbon footprint through the adoption of renewable energy, improve the energy efficiency of its operations, or practice waste reduction and recycling.

Social: The social dimension of ESG refers to how the company manages relationships with its employees, suppliers, customers and the communities in which it operates. This ranges from ensuring fair and safe working conditions to getting involved in and supporting community projects. An example of this would be implementing diversity and inclusion programs, offering training and professional development to employees, or participating in corporate social responsibility initiatives that benefit local communities.

Governance: Governance relates to the internal direction of a company, its leadership, compensation, audits, internal controls, and transparency in decision-making. Effective governance practices ensure that a company is run in a way that is ethical, legal and in line with the interests of its shareholders. This can range from implementing anti-corruption policies and transparent reporting systems to ensuring that boards of directors are diverse and act in the best interests of the company and its shareholders.

Why Adopt ESG Practices?

The integration of ESG practices into corporate strategies is not simply a passing trend; It is an essential component to ensuring the long-term success and relevance of any company. The adoption of these practices not only reflects a commitment to sustainability and social responsibility, but has also become a determining factor in competitiveness and perception in the market.

The main reason for companies to adopt ESG practices is the growing evidence that these practices lead to better performance in the long term. Companies that prioritize environmental sustainability, social responsibility and strong governance tend to have better risk management, greater attractiveness to investors and consumers, and a greater ability to innovate and adapt to changes in the market. Additionally, with an increasing focus on corporate responsibility by regulators and the public, ESG practices have become a crucial aspect of maintaining a positive corporate image and fostering consumer trust.

From a business sustainability point of view, ESG practices help companies operate more efficiently and with a lower environmental impact. This includes everything from reducing energy consumption and implementing cleaner production processes to adopting policies that promote diversity and inclusion within the organization. These practices not only reduce costs in the long term, but also put the company in a more favorable position in the face of increasingly strict environmental and social regulations.

In terms of social responsibility, ESG practices allow companies to actively contribute to the well-being of the communities in which they operate. This may include participating in community development initiatives, implementing fair labor practices, and contributing to projects that address important social challenges. Such actions not only improve the company’s reputation, but also create a more positive and sustainable environment for doing business.

ESG practices are critical for companies seeking to thrive in a business environment increasingly aware of social and environmental impacts. By adopting these practices, companies not only secure a place in the current market, but also contribute to building a more sustainable and fair future.

Corporate Transformation through ESG

The adoption of ESG (Environmental, Social, and Governance) practices by corporations is driving significant changes not only in their operations, but also in their organizational culture. This movement towards a more sustainable and responsible approach is redefining what it means to be a successful company in the current century.

ESG practices are influencing companies at multiple levels. Environmentally, they are promoting the adoption of more sustainable processes and the reduction of negative impacts on the environment. Socially, they are promoting a more fair and ethical approach in the treatment of employees, suppliers and the communities where they operate. In terms of governance, they are encouraging greater transparency and accountability in decision-making.

This change goes beyond simple adjustments in operations; represents a transformation in corporate mentality. Companies no longer focus solely on profit maximization, but also seek to generate a positive impact on society and the environment. This is reflected in a corporate culture that values sustainability, social responsibility and business ethics.

Practical Tips for Integrating ESG

The incorporation of ESG practices in companies is not only a strategy to improve their public image, but a comprehensive transformation that affects all levels of the organization. For this integration to be effective, it is important to follow a series of steps and have appropriate tools.

To successfully integrate ESG (Environmental, Social, and Governance) practices into a company, it is important to start with a detailed assessment of the organization’s current practices in relation to ESG criteria. This initial analysis is essential to identify both areas of improvement and development opportunities. Subsequently, it is important to define specific and achievable ESG-related objectives, such as setting goals for reducing carbon emissions or improving diversity in the workforce.

A key aspect in this process is the training and engagement of employees at all levels of the organization. It is essential to educate workers about the importance of ESG and how they can contribute to these goals in their everyday roles. Furthermore, it is vital that ESG is integrated into the company’s overall strategy and not simply an add-on. This means incorporating ESG principles into decision-making, strategic planning and operational processes.

To monitor progress and ensure the effectiveness of these practices, it is necessary to carry out continuous monitoring and establish clear metrics. It is also important to maintain transparent communication about the progress and challenges in ESG implementation, both internally within the company and with external stakeholders.

In terms of tools and resources, it is beneficial to use software specialized in ESG management, which allows the collection, analysis and reporting of data related to these practices. Additionally, it can be very helpful to work with ESG consultants for expert advice and guidance. Additionally, joining networks and collaborations with other companies and organizations that promote ESG practices can facilitate the exchange of knowledge and experiences.

By adopting these approaches, companies can ensure a more effective and consistent implementation of ESG practices, which will not only benefit their performance and reputation, but also contribute positively to society and the environment. Implementing ESG represents an essential step towards building a sustainable and responsible business model.

The impact of ESG practices in the business area extends beyond simple sustainable measures or social responsibility; represents a true transformation in the way companies operate and are perceived in society. Integrating ESG into operations and corporate culture not only improves long-term profitability and sustainability, but also strengthens relationships with stakeholders and positions companies as leaders in a market increasingly aware of global challenges. .

By Rodolfo Salazar, Partner BLP Guatemala | rsalazar@blplegal.com

For more information you can contact:

Juan Carlos Tristán | BLP Partner | jtristan@blplegal.com

10-11-2023 | Noticias-en

The Legislature of the province of Río Negro approved the law that complements the National Law of Minimum Budgets for Adaptation and Mitigation to Climate Change No. 27,520, through which provincial actions and strategies for the adaptation and mitigation of climate change are established. with the aim of protecting the inhabitants, the environment and contributing to sustainable development.

Establishes that the Provincial Action Plan against Climate Change is the base instrument for implementing the provincial policy to respond to climate change. Defines the specific actions necessary to achieve the objectives established by the policy. It is made up of a Provincial Mitigation Plan and a Provincial Adaptation Plan. It contains the goals, actions, execution schedule, evaluation mechanisms and necessary budget.

The Plan contains at least:

a. An analysis of the changes observed in the main present and future climate variables.

b. The identification and evaluation of current and future climate risk according to climate threats, vulnerability, and adaptive capacity of people, ecosystems and infrastructure.

c. The identification of critical regions, sectors, activities and climate risk groups.

d. A qualitative and quantitative goal of the necessary adaptation efforts.

and. A quantifiable, anthropic, fair and ambitious emissions reduction goal.

F. The survey of government actions with an impact on the climate change mitigation and adaptation strategy, as well as review mechanisms for said actions.

g. Mitigation and adaptation actions necessary to achieve the planned goals. Description of the monitoring processes, evaluation of actions and definition of baselines and indicators.

Also, the enforcement authority will establish, within the period established by the regulations, measures and actions that seek to limit the magnitude or rate of global warming and its related effects. Mitigation actions include, but are not limited to:

a) Development and implementation of renewable and low-emission energy sources.

b) Promotion of energy efficiency in all sectors of the economy.

c) Promotion of carbon capture and storage, including reforestation and improvement of forest management.

d) Establishment of measures to reduce emissions in the transportation sector, including the promotion of low-emission modes of transportation.

e) Implementation of sustainable waste management programs to reduce emissions from waste management.

f) Development of carbon credit systems that encourage the reduction of emissions.

g) Promotion of sustainable agricultural and land management practices that contribute to the reduction of greenhouse gas emissions.

h) Application of technologies and practices that reduce greenhouse gas emissions in the construction industry.

The mitigation strategy will be governed by the principle of progressivity, taking into account the efforts established in the international framework and the specific contribution to the contribution determined at the national level.

On the other hand, it establishes that the Climate Change Cabinet may establish a Carbon Emissions Credit System based on the creation of measurable units, called carbon credits, that represent a reduction or elimination of greenhouse gas emissions. Each credit corresponds to one ton of carbon dioxide equivalent that has been avoided or extracted from the atmosphere. Entities, whether public or private, can generate carbon credits through projects that reduce greenhouse gas emissions or increase the capacity of carbon sinks. The regulations will determine the percentage of income obtained through the sale of Carbon Emissions Credits generated by provincial public projects that will be allocated to the Climate Action Fund of the Province of Río Negro.

Likewise, it provides that the province, municipalities and development commissions promote the generation, conservation and restoration of carbon sinks, prioritizing, as far as technically and economically viable, the use of native species.

For more information contact:

Gustavo Papeschi | Partner of Beccar Varela | gpapeschi@beccarvarela.com

24-10-2023 | Noticias-en

On October 12, 2023, the President of the Republic of Paraguay signed and promulgated Law 7190/2023 on Carbon Credits. The new regulations provide the country with a specific regulatory framework for the development of projects that generate carbon credits for their commercialization in international markets, whether mandatory or voluntary.

Among other provisions, the new law designates the Ministry of the Environment and Sustainable Development (MADES) as the enforcement authority and creates the national Carbon Credit Registry, which will seek to provide order and transparency to the local market and avoid double accounting of emissions reductions. . Likewise, the standard contemplates measures to safeguard compliance with Paraguay’s Nationally Determined Contributions (NDC), including the obligation to retain between 3 and 10% of the carbon credits generated by each project, and measures designed to promote knowledge transfer to Paraguayan professionals and technicians. In order to encourage national and foreign investment in local projects, the law grants certain legal protections to properties destined for projects under development, providing legal clarity to the ownership and transferability of carbon credits, and exonerating the Value Added Tax. (VAT) the transfer of these.

MADES, as the designated enforcement authority, is now tasked with regulating and implementing the specific procedures required in the new law and ensuring compliance therewith.

Paraguay, with its 16 million hectares of forests, with the accelerated increase in its forest plantations, and with its vast availability of clean and renewable hydroelectric energy, has enormous potential for the international carbon credit market, whose global value in In 2023 it is estimated at about 1.2 trillion dollars, an amount that is estimated could double in the next 5 years.

FERRERE advises local and foreign clients, including landowners, project developers, investors, specialized funds, and end buyers, in the most significant transactions in the carbon credit market in Paraguay.

For more information contact:

Carla Arellano | Counselor Ferrere | carellano@ferrere.com

23-10-2023 | Noticias-en

Through Executive Decree No. 754 of May 31, 2023, President Guillermo Lasso reformed the Regulations to the Organic Code of the Environment (hereinafter, “RCODA”).

This reform is preceded by Sentence No. 22-18-IN/21 of September 8, 2021, in which the Constitutional Court: (i) Clarified that the environmental consultation and the prior consultation with indigenous communities are different consultations, and that Art. 184 of the CODA does not apply or replace the right to prior consultation of indigenous communities; (ii) Ordered that Art. 184 of the CODA must be interpreted according to the Constitution of the Republic, the jurisprudence of the Constitutional Court, and the Escazú Agreement;[1] (iii) Declared the unconstitutionality of Arts. 462 and 463 of the RCODA; and (iv) Ordered the President to adapt the RCODA to what was resolved. Subsequently, the aforementioned Court issued Ruling No. 1149-19-JP/21 of November 10, 2021, in which the right to environmental consultation was developed.

The main reforms carried out by Decree No. 754 are the following:

1. The citizen participation process is reformed. This will no longer be governed by the technical standard of the Environmental Authority but by that established in the RCODA, below. Furthermore, the majority opposition of those consulted is regulated, indicating that it is not binding. However, it is established that, if the environmental permit is granted despite majority opposition, it must be duly motivated.

2. All regulations in the RCODA regarding prior consultation with indigenous communities are repealed and Title III of Book III of the RCODA on the citizen participation process for environmental consultation is reformed:

2.1. It is established that the right to environmental consultation will consist of informing the community “about the content of the environmental technical instruments, the possible environmental impacts and risks that could arise from the execution of the projects, works or activities, as well as the relevance of the actions to be taken”, record and compile your criteria, opinions and observations, and thereby consult you about the granting of the corresponding environmental permit.

2.2. It is added that the rules on the citizen participation process for environmental consultation are mandatory and apply in the case of an environmental license, always, and in the case of environmental registration for activities in the hydrocarbon and mining sector.

23. It is established that the citizen participation process for environmental consultation must be carried out prior to the granting of environmental permits. Additionally, the following changes are added to the process:

2.3.1. The Ombudsman’s Office must be notified so that this entity can proceed to provide support to the community and monitor the process. Your participation is mandatory, however, your unjustified absence will not lead to the nullity of the process.

2.3.2. The operator of the project, work or activity must deliver to the competent Environmental Authority the technical environmental instruments that it requires, as well as all the communication materials or supplies for the didactic dissemination of such instruments (e.g. summaries, brochures, slides, etc. ). All deliverables must be translated, when applicable.

2.3.3. To carry out the process, citizen participation mechanisms will be used, including the following: (i) Information mechanisms (e.g. information assemblies, electronic pages, information videos, delivery of information documentation on environmental technical instruments, public information centers, workshops of environmental socialization; (ii) Call mechanisms (e.g. public call, personal invitations); and (iii) Consultation mechanisms (Consultation Assembly).

2.3.4. Special provisions are included to consider when the consultation is carried out in the territories of indigenous peoples: provisions related to their ancestral languages and their forms of organization and decision-making.

2.3.5. The operator of the project, work or activity will be the one who must finance the environmental consultation process, its call and the logistics. He must also provide all the facilities and provide all the resources necessary for its execution.

2.3.6. The process will be divided into two phases: (i) Information Phase and (ii) Consultative Phase. In the first, the delivery of information occurs. In the second, a dialogue takes place between the State and the community in order to present the opinions and observations of the community and consult regarding the issuance of the environmental permit.

3. The validity of all environmental permits that were issued before the reform is ratified. On the other hand, any project, work or activity registered in the SUIA until October 11, 2021 will follow the process prior to the reform. This reform will continue the processes initiated at a later date, even if they have received a technical ruling, as well as the projects, works and activities of the mining sector blocked in the SUIA by Sentence No. 1149-19-JP/21.

For more information contact:

Maria Rosa Fabara | Partner Bustamante Fabara | mrfabara@bustamantefabara.com