The Federal Economic Competition Commission (“COFECE”), published on November 23, 2022, the initiation of the investigation with file number IEBC-004-2022, for possible barriers to competition and essential inputs in the distribution and commercialization of corn, as well as the production, distribution and commercialization of corn flour and related services in the national territory.

Regarding this investigation, COFECE explained that this market is particularly important because corn and corn flour are necessary inputs for the production of tortillas, which form an essential part of the daily diet of Mexicans, since around 98.6% of the population consumes it and it is included in the basic basket.

In accordance with the Federal Economic Competition Law, once the investigation is concluded and sufficient elements are found to determine the existence of barriers to competition and free competition, COFECE may: (i) order the removal of barriers that unduly affect the process of competition and in case of non-compliance, impose a sanction of up to 10% of the income of the economic agent, (ii) issue recommendations to public authorities, (iii) determine the existence of essential inputs and, where appropriate, issue guidelines for its regulation, and (iv) order the disincorporation of assets, rights, social interests or shares.

In this investigation, COFECE may request information in writing, carry out verification visits, as well as summon economic agents that participate in or are related to said market to testify.

In 2019, the Ministry of Environment and Natural Resources decreed a 3-year extension to the period for regularization of environmental instruments in Guatemala contained in Government Agreement 237-2016. Thus, existing projects have until December 16, 2022 to request their respective environmental license, under penalty of a fine ranging from Q5,000 to Q100,000.

The environmental instrument is a technical document that establishes the environmental impacts or risks and the actions that will be carried out to mitigate those damages; Said instrument is approved through an environmental license. The obligation to have an environmental instrument exists since 1986 according to article 8 of the Law for the Protection and Improvement of the Environment (Decree 68-86).

In 2016, the Environmental Control and Monitoring Regulation -RECSA-, Government Agreement 137-2016, was issued, setting a two-year term for companies to regularize by presenting their environmental instrument.

Due to the large number of interested parties who decided to regularize their situation, on December 24, 2019, the reform to RECSA was published in the Diario de Centroamérica and established two important modifications:

A term of 3 more years (expiring on December 16, 2022) was set for the process of regularization of environmental instruments, with the imposition of a fine of Q. 5,000.00 regardless of the category of the project.

The obligation to present a bond or better known as surety insurance, which was a requirement to obtain an environmental license, was eliminated.

Let us remember that the purpose of all of the above implies being in compliance with local legislation, guaranteeing the protection of our environment and seeking to mitigate the damage that we produce.

Recently, the Perú Libre Parliamentary Group presented Bill No. 3251/2022-CR, whose purpose is to regulate the responsibility of companies in the Financial System, with respect to computer fraud committed against users of this system in the face of active and fraudulent liabilities, establishing the actions that must be taken and determining the times for the resolution of the cases.

The purpose of said bill is to protect and guarantee active and passive operations carried out by users of the financial system, reducing economic damage and safeguarding good credit reputation.

Among the measures contemplated in the proposed standard, the obligation is prescribed for companies in the financial sector to return the amounts and/or cancel unauthorized operations reported by their users, in any case and no later than the business day following reported the incident. If the company has reasonable grounds to doubt the veracity of the report, it must inform the user and the Superintendency of Banking, Insurance and AFPs in writing, within the same term, attaching the evidence that supports its position, and it is the responsibility of the company to demonstrate that for said operation, all the verification mechanisms were activated that demonstrate that said operation was correctly registered.

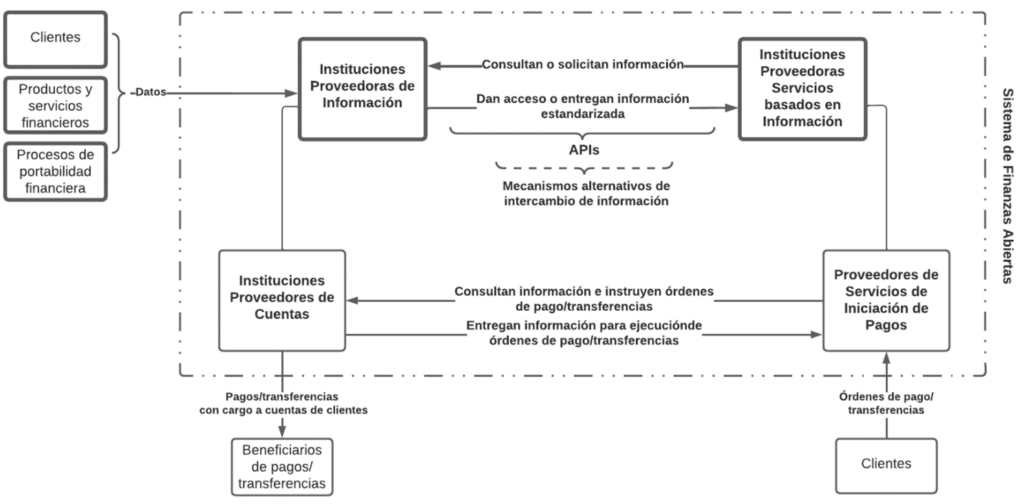

The recently approved Fintec Law creates the Open Finance System (SFA), whose objective is to promote competition, innovation and inclusion in the financial system, facilitating the exchange of information between different service providers in this field.

This will occur through remote and automated access interfaces–known as application programming interfaces or “APIs”—, which will enable direct interconnection and communication between said providers without the need for a contractual relationship that binds them.

The SFA will function under the supervision and oversight of the Commission for the Financial Market (CMF) . It will correspond to it to dictate the regulation and instructions necessary for its adequate implementation and operation, as well as to supervise the fulfillment of the obligations of its participating institutions.

Below, we describe the main aspects of the operation of the OSS, including the information it will contain, the institutions that will participate in it and their roles, and the main deadlines established by law.

What kind of information will be exchanged?

The Fintec Law establishes a non-exhaustive list of information that must be exchanged through the SFA:

Information on general terms and conditions of financial products and services, and on customer service channels.

Identification information and registration of clients of financial products and services and their representatives.

Information on the commercial conditions contracted and the history of transactions of clients of financial products and services, such as checking, sight, provision of funds and savings accounts, credit cards, insurance policies, savings or investment instruments and operation services cards and similar means of payment.

Communications between financial providers for purposes of financial portability.

Data or information necessary for the provision of payment initiation services.

Other data or information related to financial products or services or initiation of other types of transactions that the CMF may define through a general rule.

While the information in points (i) and (iv) must be available in open data formats, that in points (ii), (iii), (v) and (vi) may only be shared to the extent that the respective clients have previously authorized it.

2. What type of institutions will participate?

The Fintec Law defines 4 categories of participating institutions:

Information Provider Institutions – are those that generate the information that will be available through the OSS, so their participation is mandatory. This category includes, among other institutions, banks, issuers and operators of cards or other means of payment authorized by the CMF, savings and credit cooperatives, insurance companies, general fund managers, stock brokers and compensation funds.

Information-Based Service Provider Institutions – are those that may consult, access and receive data from the Information Provider Institutions through the OSS. Although their participation is voluntary, as a general rule they must register in advance in a special registry in charge of the CMF. As an exception, duly authorized Information Provider Institutions and Financial Service Providers will not require new registration, but they will be subject to compliance with the same requirements applicable to entities whose participation is voluntary.

Payment Initiation Service Providers – are those that provide services to clients holding checking, sight or fund accounts, consisting of the instruction (on behalf of these clients and before Account Provider Institutions) to execute payment orders or transfers electronic funds charged to their respective accounts and means of payment. To operate legally, these entities must be registered in a special registry in charge of the CMF.

Account Provider Institutions – are the banks and financial institutions that provide checking, sight or fund accounts. Although they already qualify as Information Provider Institutions, the Fintec Law has specifically defined them to regulate their relationship with Payment Initiation Service Providers within the framework of the SFA. Their participation in the latter is therefore mandatory.

Diagram No. 1. Roles of the institutions participating in the OSS.

3. Will there be charges associated with its operation?

Information Provider Institutions may not charge Information-based Service Providers for the communication of customer data information requested through the SFA APIs. This, with the exception of the reimbursement of the direct incremental costs that must be incurred to meet the number of requests over the thresholds that the CMF must define based on public, objective, equitable and non-discriminatory conditions among the participating institutions.

The aforementioned requests for information may not give rise to the collection of commissions or additional charges to clients.

4. When will you start operating?

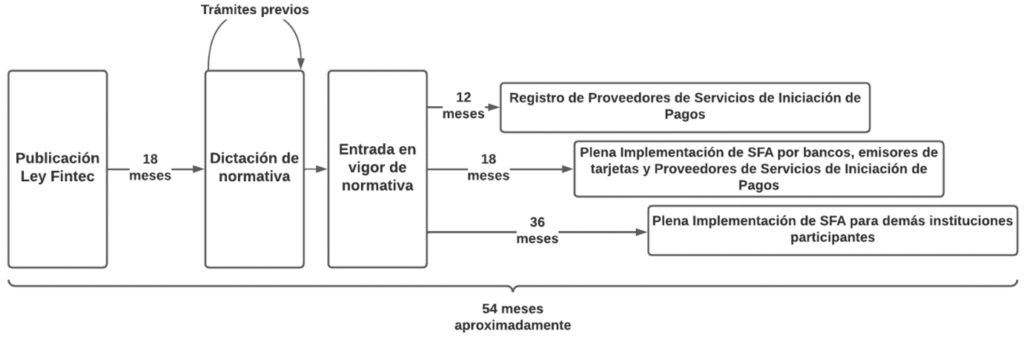

The CMF must issue the necessary regulations for the gradual implementation of the OSS within a period of 18 months from the publication of the Fintec Law in the Official Gazette. This regulation will be subject to prior public consultation procedures, regulatory impact assessment and reports from the National Economic Prosecutor’s Office.

Although the process will be gradual, the Fintec Law has also established certain maximum deadlines to complete the implementation. Counted from the entry into force of the regulations issued by the CMF, there will be 12 months for the registration of the entities that on the date of entry into force of the Fintec Law are providing Payment Initiation Services; 18 months for the full operation of the OSS in banks, card issuers and Payment Initiation Service Providers; and 36 months for full operation in the other participating institutions.

Diagram No. 2. Main terms of the SFA.

The SFA means a relevant step for the country on the path of open finance , so it is foreseeable that its operation will entail significant challenges for the participating institutions. Do not hesitate to contact us if you want to know more about the Fintec Law or its related topics.

For more information contact:

Natalia Gonzalez | Associate Group az Tech | ngonzalez@az.cl

On December 1, the Assembly No. 102 of the Federal Consumer Council (Cofedec) will be held in Paraná, organized by the General Directorate of Consumer Defense and Commercial Loyalty of Entre Ríos.

Officials of the National Secretariat of Commerce, of the Undersecretary of Actions for the Defense of Consumers and of the National Directorate of Consumer Defense and Consumer Arbitration, as well as directors of Consumer Defense from all over the country, They will participate in the assembly to deepen and coordinate policies and actions related to consumer rights and commerce.

The Federal Consumer Council is a body for coordinating policies related to issues related to consumers. It is made up of representatives of the National Government, the Autonomous City of Buenos Aires and all the provinces. In each of the Assembly, projects are debated and policies related to consumer issues are coordinated, where the national authority and the provincial authorities share experiences and develop policies together in order to defend and strengthen the rights of consumers.

The province of Entre Ríos, in addition to being a member of Cofedec, is part of the Agency’s body of Advisors on issues related to Consumer Education, by democratic election of all the member provinces.

In the last two assemblies that took place in Rosario, Santa Fe and Resistencia, Chaco, key issues will be addressed such as: competence of the Central Bank of the Argentine Republic in relation to financial consumption relations; direct damage and savings plans: National Insurance Superintendency; setting of general administrative procedures; sales through social networks; prepaid medicine: pre-existing, disability cases; competencies in aeronautical issues: referral to the National Civil Aviation Administration; banking problems: bank account blocking and abusive debt refinancing; credit card: summary challenge for charges revoked in a timely manner; among others.

The following are functions of the Federal Consumer Council:

a) Promote consumer or user education with the objectives of:

I) Strengthen freedom of choice and optimize rationality in the consumption of goods and services,

II) facilitate the understanding and use of the information provided to users and consumers by providers,

III) disseminate knowledge of the duties and rights of consumers and users and the most appropriate way to exercise them and,

IV) promote the prevention of risks that may arise from the consumption of products or the use of services.

b) Promote the homogenization of criteria regarding the application of public policies related to consumption, including proposals for modification and/or harmonization of current regulations on consumer protection.

c) Exchange information with the productive sectors in order to promote greater efficiency in the production and marketing of goods for consumption.

d) Promote the installation of public consumer or user information offices that fulfill at least the following functions:

I) disseminate the results of studies, comparative analyses, tests and quality controls on products and services and,

II) manage the reception, registration and acknowledgment of receipt of complaints and claims from consumers or users and their referral to the corresponding entities or agencies.

e) Stimulate the creation of consumer associations, maintaining a permanent exchange and collaboration with them and keeping updated national and provincial records of existing ones.

f) Collect information from public and private entities related to consumer protection.

g) Request the collaboration of the control entities and organisms with competence in the matter for a better attention to the problems of consumers and users.

h) Request the collaboration of public and private institutions, specialized departments of universities and any other technical body to carry out studies, comparative analyses, tests and quality controls on products or services and disseminate their results.

i) Propose to the competent authorities the granting of scholarships for the personnel affected by the departments, for the purpose of their permanent training in the matter of consumer protection.

j) Promote the exchange of information and collaboration to carry out actions aimed at consumer protection with international public and private consumer defense organizations.

k) Provide advice to the National Congress and the Provincial Legislatures regarding problematic consumer legislation.

l) Strengthen institutional relations with other official bodies with competence in consumption or regulatory bodies for public services.